In 2024, S&P Global Ratings upgraded Oman’s sovereign credit rating from “BB+” to “BBB-” with a stable outlook, marking the Sultanate’s return to investment-grade status after nearly seven years. As of 2026, S&P reaffirmed Oman’s “BBB-” rating with a stable outlook, reflecting continued improvements in public finances, fiscal discipline, debt reduction, and the sustained implementation of economic reforms.

In 2025, Oman’s economy demonstrated stronger growth of 2.4%, compared to 1.6% in 2024, supported by structural reforms and continued diversification efforts under Vision 2040. Petroleum activities grew by 1.1%, primarily driven by a 1.2% increase in crude oil activities. Meanwhile, the non-oil economy expanded by 3.2%, supported by strong performance across the services, construction, mining, and agriculture and fishing sectors. The medium-term outlook remains positive, with the International Monetary Fund projecting Oman’s economy to grow by 3.5% in 2026, supported by stable non-oil activity, gradual recovery in hydrocarbon production, and the continued implementation of fiscal and structural reforms.

Oman’s fiscal and external positions remained resilient in 2025, supported by disciplined fiscal policies, improving non-oil revenues, and continued debt reduction efforts. Oman’s 2025 budget, which was based on a conservative oil price assumption of US$60 per barrel, initially projected a fiscal deficit of 620 million. However, preliminary data released in early 2026 indicated that the deficit narrowed significantly to approximately

620 million. However, preliminary data released in early 2026 indicated that the deficit narrowed significantly to approximately  480 million (US$1.2 billion), supported by stronger-than-expected revenue generation, with excess proceeds utilized toward public debt reduction. S&P Global Ratings expects Oman to achieve fiscal balance in 2026 and projects relatively stable fiscal surpluses averaging around 0.4% of GDP during 2027–2029. Meanwhile, the current account is expected to remain broadly balanced, with modest surpluses of around 2.0%–2.3% over the medium term. Public debt continued to decline, falling below 35% of GDP in 2025, with further improvement expected, reflecting the government’s sustained commitment toward strengthening fiscal sustainability and reducing economic vulnerabilities.

480 million (US$1.2 billion), supported by stronger-than-expected revenue generation, with excess proceeds utilized toward public debt reduction. S&P Global Ratings expects Oman to achieve fiscal balance in 2026 and projects relatively stable fiscal surpluses averaging around 0.4% of GDP during 2027–2029. Meanwhile, the current account is expected to remain broadly balanced, with modest surpluses of around 2.0%–2.3% over the medium term. Public debt continued to decline, falling below 35% of GDP in 2025, with further improvement expected, reflecting the government’s sustained commitment toward strengthening fiscal sustainability and reducing economic vulnerabilities.

Inflation remained moderate in 2025, averaging around 1.0%, with stable housing and utility costs helping contain overall price pressures despite moderate increases in transportation and selective food categories. The Omani rial’s peg to the US dollar continued to support price stability effectively.

Oman’s government is actively implementing reforms aligned with Vision 2040, including improving the business environment, enhancing labor market flexibility, and accelerating digital and green initiatives. However, risks remain, including global oil price volatility, geopolitical uncertainties, and potential delays in structural reform execution. Nonetheless, Oman’s outlook is increasingly stable, supported by improved credit ratings and growing investor confidence.

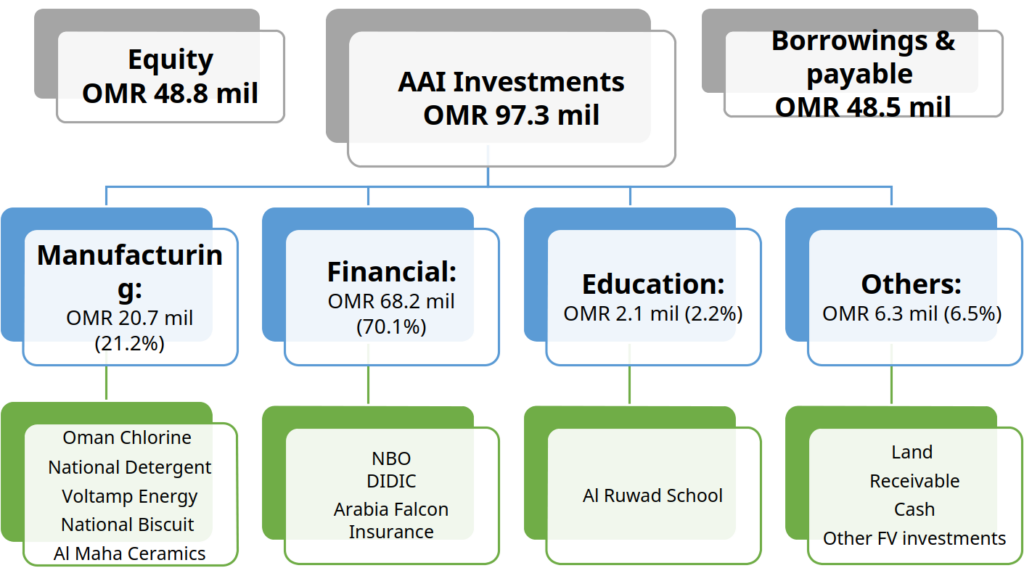

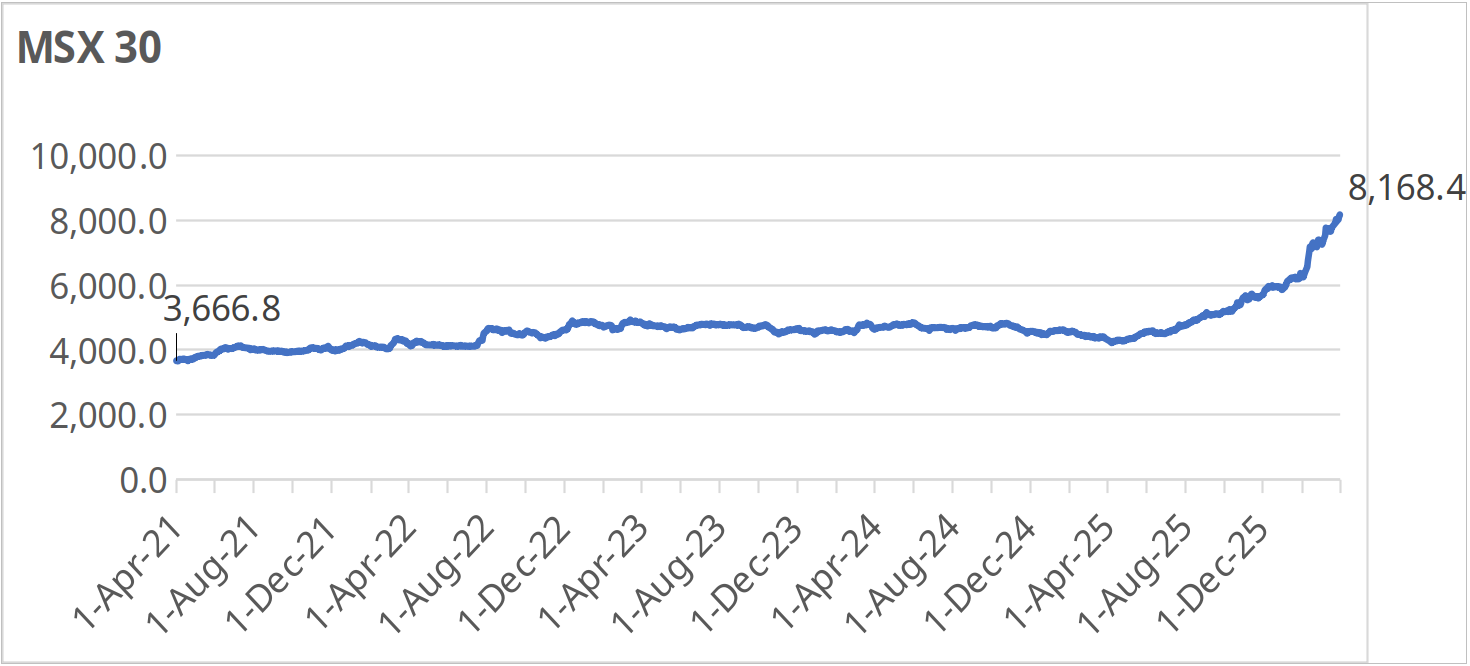

In the year 2024-25 AAI Board approved 5-year strategy aims to increase its asset base to 100 million. The strategy focused on the following key objectives:

New investment in growth sectors:

AAI aims to capitalize on new opportunities, with a primary focus on the banking sector. Over the past two years, the Company has significantly increased its exposure to this sector—from 2% to 55% of total assets. This strategic shift has delivered strong results, including enhanced returns, higher dividend income, and improved portfolio diversification.

Beyond banking, AAI is also targeting select investments in the industrial sector. The focus will be on businesses expected to benefit from an improving economic environment, particularly in building materials, chemicals, equipment manufacturing, food manufacturing, and fast-moving consumer goods (FMCG). These sectors are well-positioned for long-term growth and align with AAI’s objective of generating sustainable value across its portfolio.

Enhance profitability of associate:

AAI as an active investor is committed to enhancing the profitability of its associate by supporting the boards of its associate companies in implementing strong corporate governance, improving senior management capabilities, and optimizing operational costs. The strategy also focuses on expanding business capacity, pursuing mergers and acquisitions, and forming strategic partnerships to drive growth and foster synergies. As a result of the above initiatives and due to other favorable outcomes, the profits from a number of AAI associate companies have improved substantially in the last 3 years. Several other initiatives are currently being executed by each of AAI associate companies which should lead to further enhancements of profits within the next 5 years.

Divestment and Portfolio Diversification:

AAI continuously evaluates its investment portfolio to optimize risk-adjusted returns and enhance long-term shareholder value. As part of its active portfolio management approach, the Company selectively reallocates capital from certain mature investments into opportunities that offer stronger long-term growth potential and improved portfolio diversification. In line with the strategy, AAI fully divested its holding in Bank Dhofar during the year.